Lesson 3: Risk Engine - Position Sizing, Stops, and R-Multiples

Beginner LevelPublished: September 15, 2025

Lesson 3: Risk Engine - Position Sizing, Stops, and R-Multiples

Learning outcomes: Protect capital, size every trade correctly, and measure performance in R.

Risk is the only part you control. If you control risk, you control survival and long-term compounding.

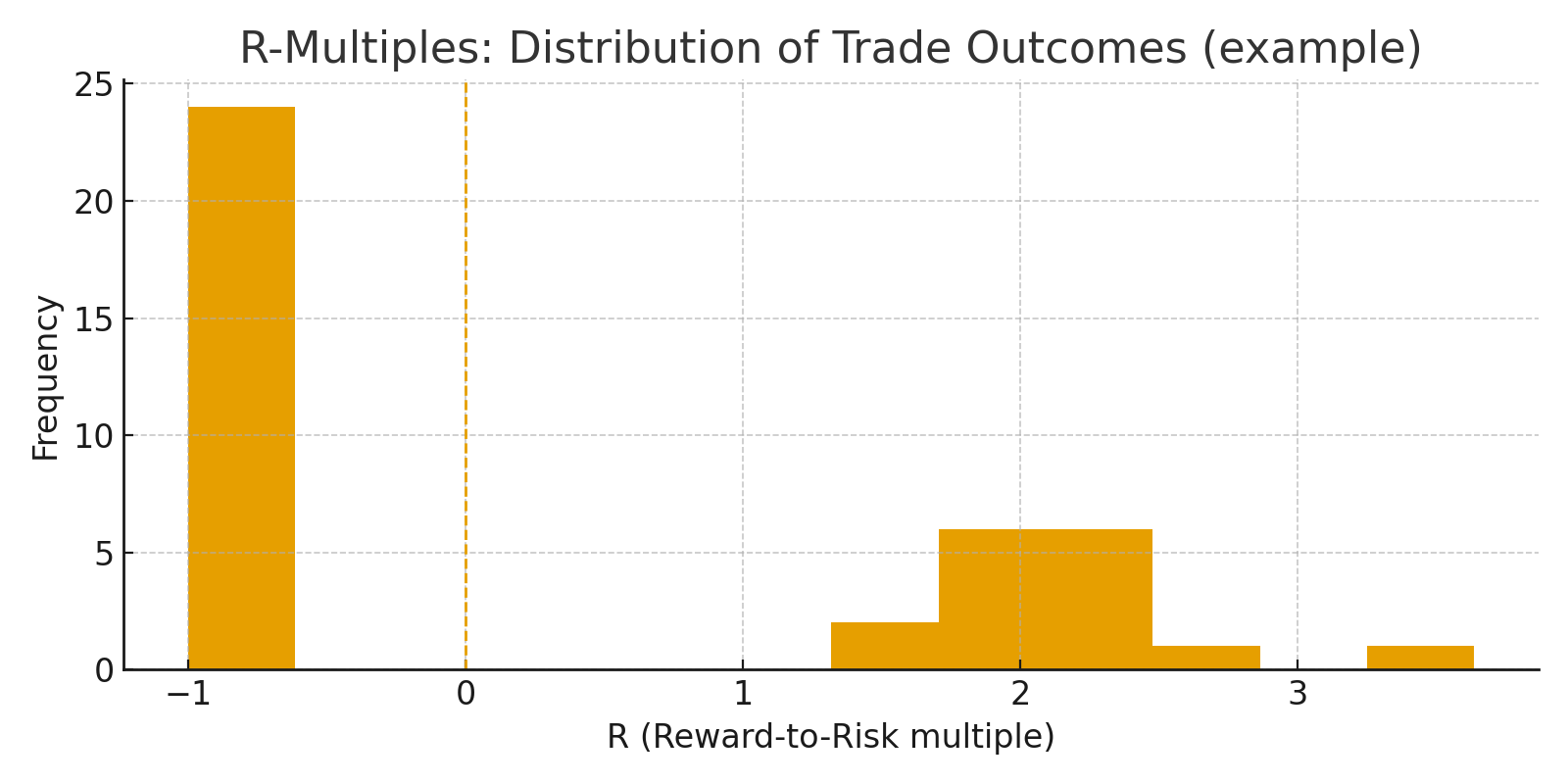

R-multiples let you compare trades without emotion. A win is only a win if it beats your risk.

Core concepts

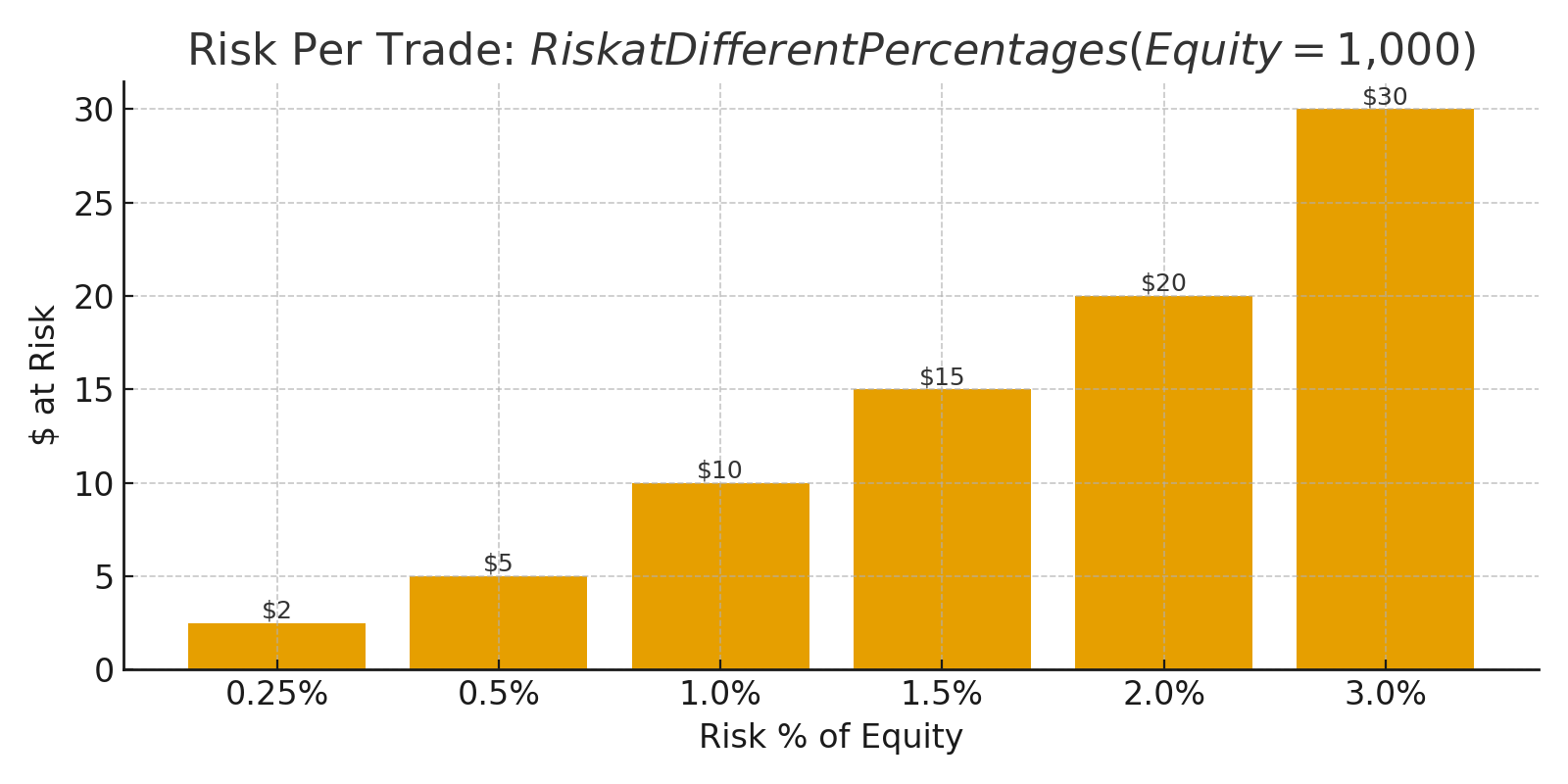

- Fixed fractional risk (0.5 to 1.0 percent while learning).

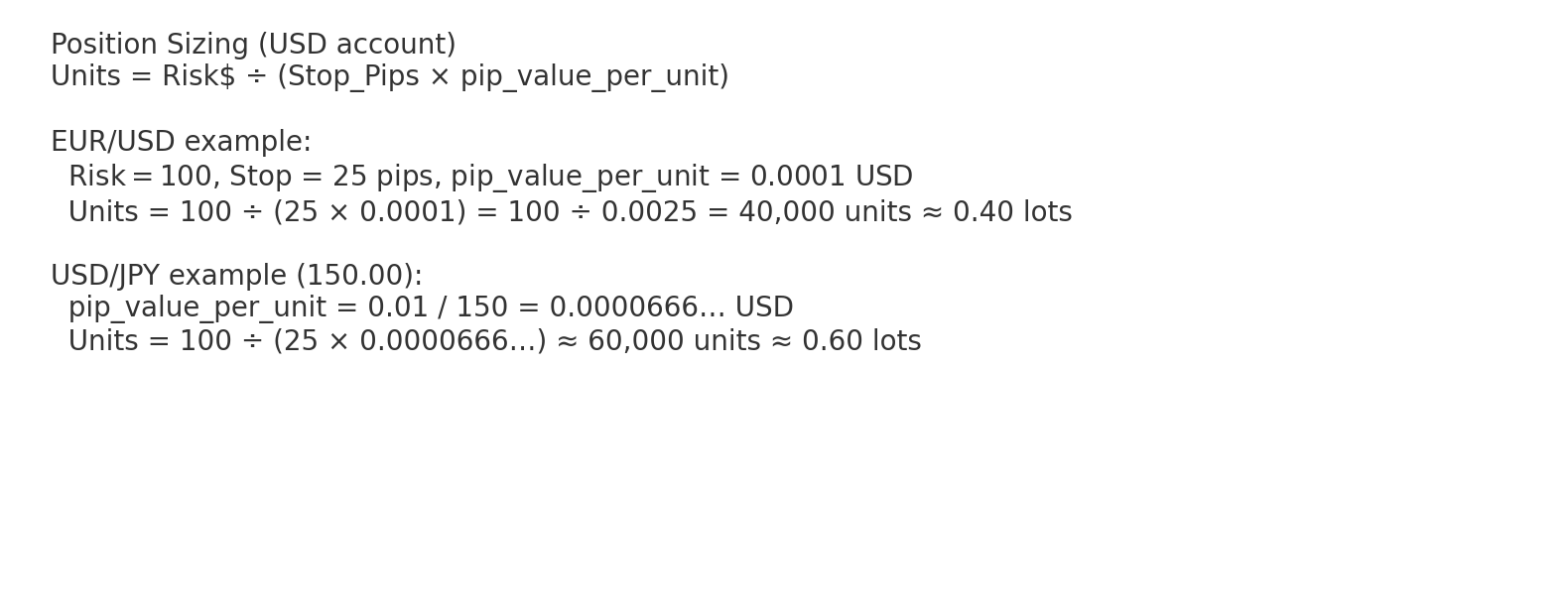

- Position sizing = Risk / (Stop pips x pip value).

- Stops placed beyond invalidation, not inside the zone.

- ATR to validate stop distance.

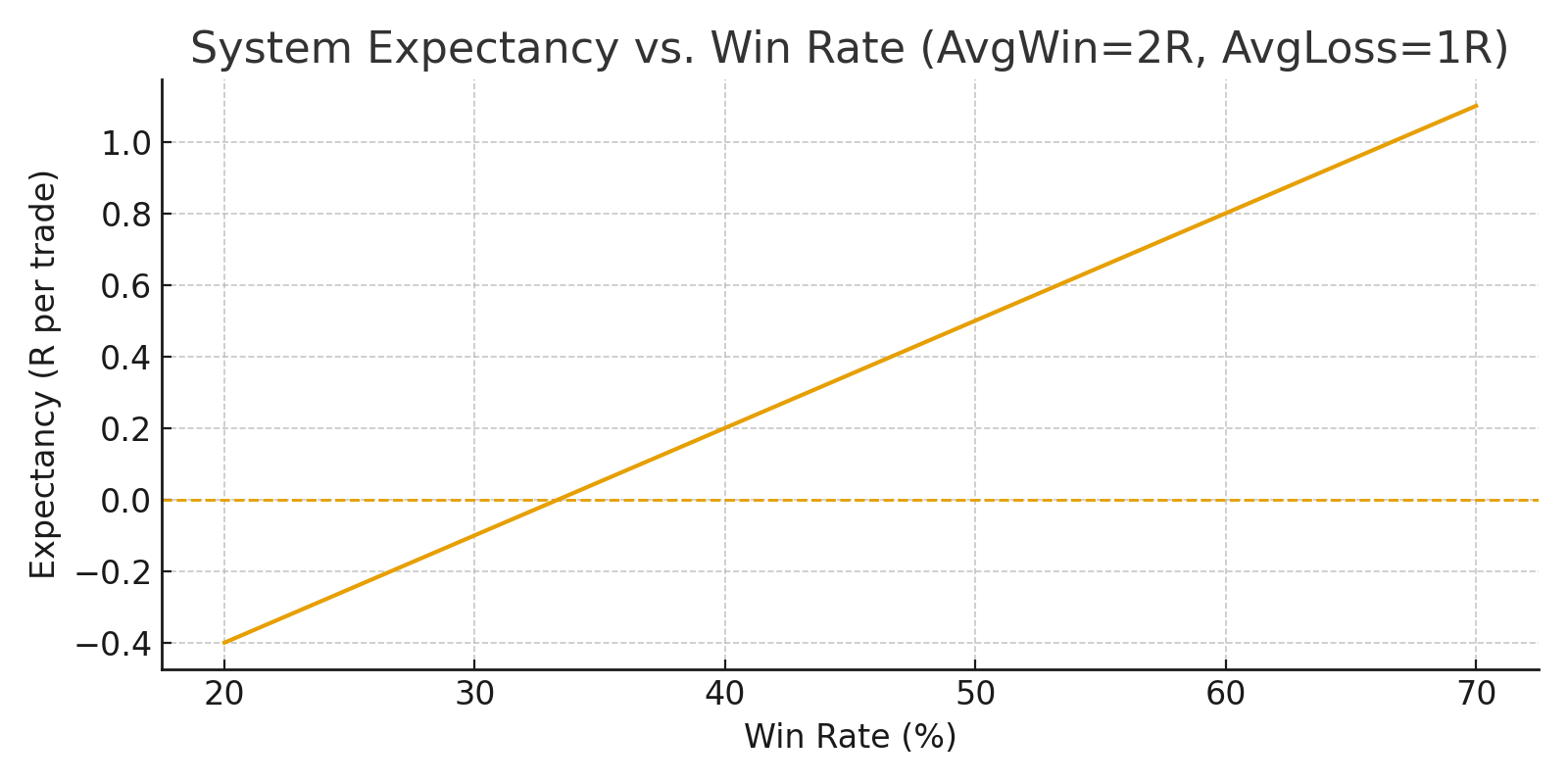

- Expectancy = win rate x avg win - loss rate x avg loss.

Execution framework

- Define your risk per trade.

- Find the invalidation level and set the stop.

- Compute position size using the formula.

- Define the target in R (start with 1.5 to 2R).

- Log the trade in R after it closes.

Annotated walkthrough

Example: GBPJPY with a 30 pip stop and 1 percent risk.

- Risk 1 percent of account balance.

- Stop is 30 pips beyond the invalidation level.

- Size the trade so 30 pips equals 1 percent risk.

- Target 2R to keep expectancy positive.

Common mistakes

- Moving stops to avoid a loss.

- Increasing size after a loss.

- Ignoring spread and slippage in your risk.

- Tracking P/L in dollars instead of R.

Checklist

- Risk percent defined.

- Stop beyond invalidation.

- Position size calculated.

- Target set in R.

- Max daily loss rule set.

- Trade logged with R outcome.

Practice drills

- Calculate size for 5 different stop sizes.

- Backfill 10 trades and compute average R.

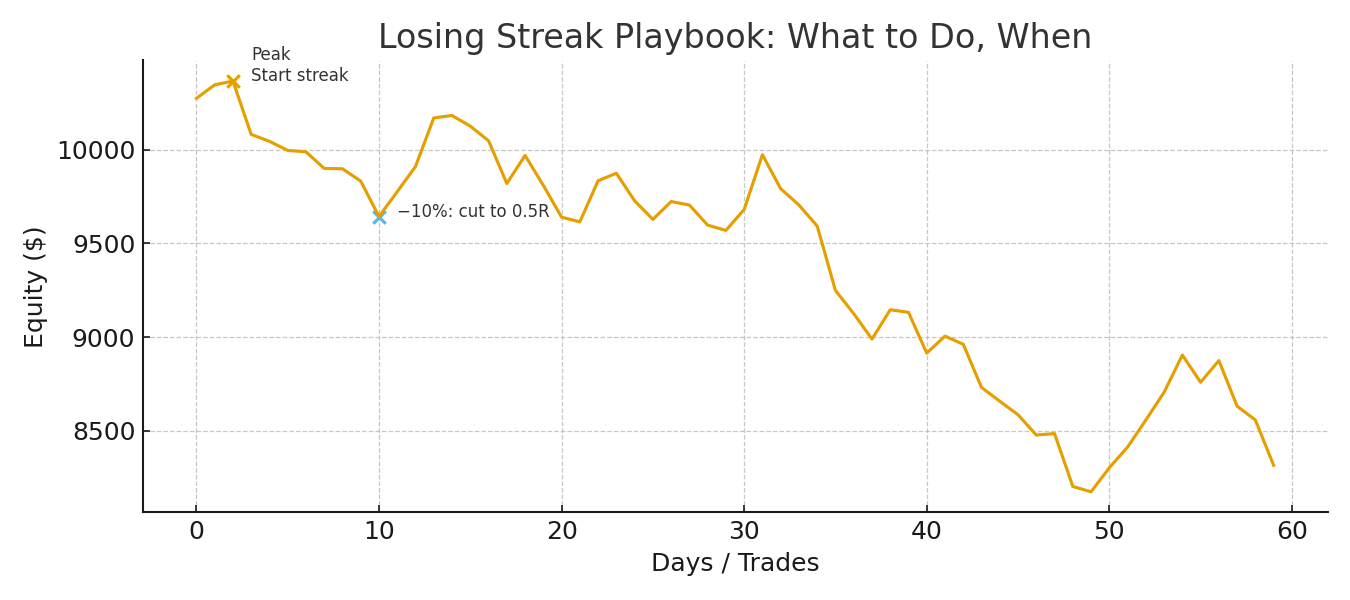

- Simulate a 5 loss streak to confirm risk tolerance.

Pro tips

- Consistency beats intensity.

- R-multiples remove emotional bias.

- Never let one trade decide your month.

Annotated Chart Pack

5+ annotated examples for this topic.

Download the lesson pack for offline study and practice.

Lesson Quiz

Pass mark: 80%